TL;DR – Listen to the article post:

Because open discussions about money are considered taboo, and comparing your own personal financial situation to your friends isn’t very effective, it can be difficult to know where you stand financially. One of the most useful (and simple) metrics to gauge your financial health is your net worth.

Net Worth = Assets – Liabilities (i.e. Debts)

Assets are anything of value that you own that can be turned into cash (house, car, cash, stocks, etc.). Liabilities are debts that you owe to others (mortgage, car loan, credit card debt, student loans, etc.). The difference between the two is how much you really own — your net worth.

Net worth is a snapshot of your current financial position and the product of everything you’ve saved and spent up until now.

For example, if you put all of your savings into vintage baseball cards and had a collection worth $100,000 but also had $50,000 of student loan debt, you would have a net worth of $50,000.

While I’m not a big fan of comparisons because everyone’s situation is different, I do think it can be useful on occasion to use an objective benchmark like net worth to get a sense of where you’re at.

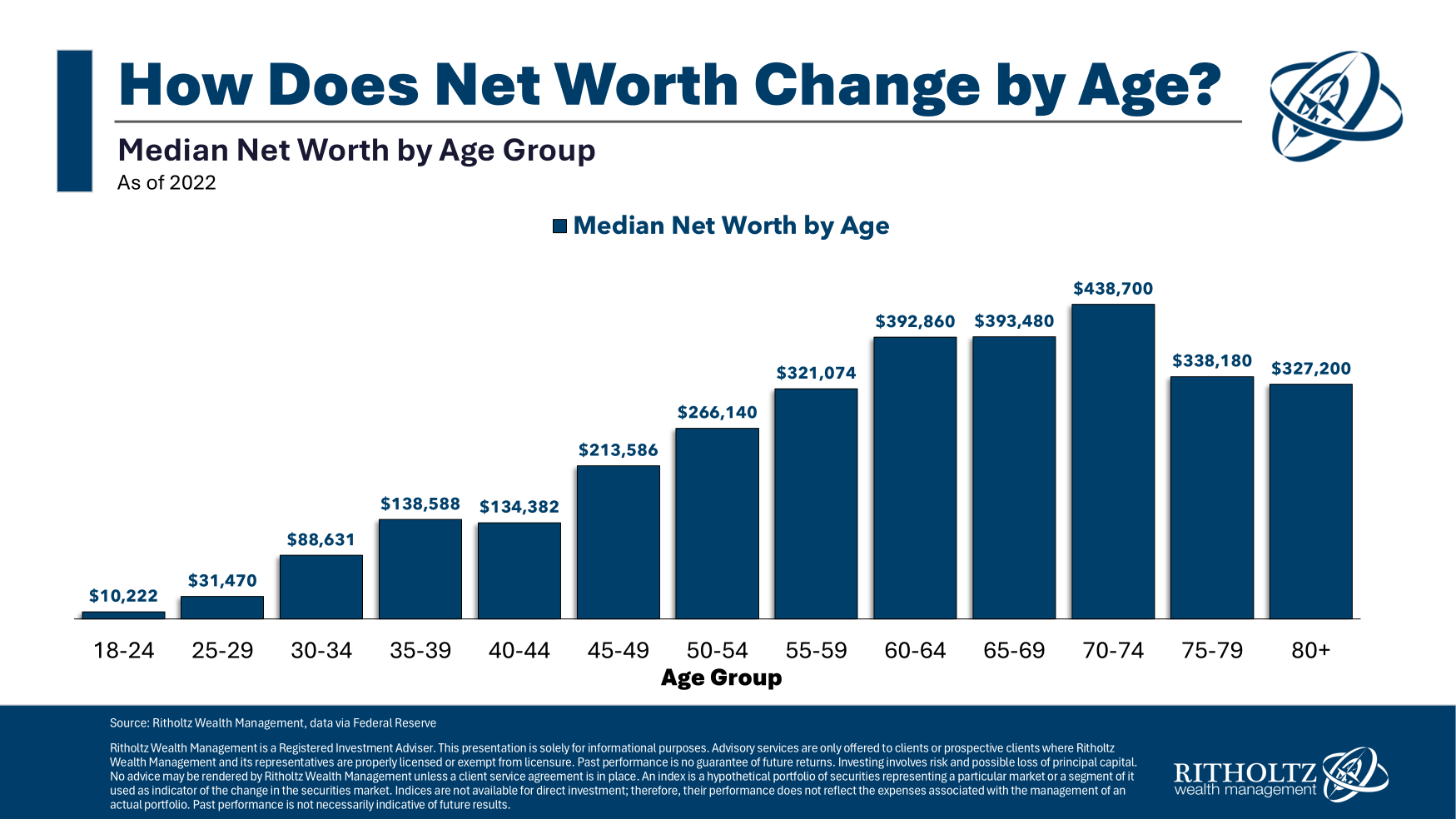

The following chart shows the median net worth levels in America, sorted by age:

The issue with data like this is we’re far more interested in how we compare to our friends and neighbors than to the median.

Also, there is a wide range around these median numbers. In the 40-44 age group, median net worth is $134,000. But for the bottom 25% it’s $23,000. For the top 25% it’s $436,000. And for the top 10% and 1%, net worth is $1.1 million and $7.8 million.

If you’re worried about where your net worth stands right now, keep in mind that it may not tell your whole story, especially if you’re young. You could have a low or negative net worth simply because you’re early in your career, or maybe you decided to take out student loans to help boost your earning potential and therefore increase your net worth even more down the road.

So, perhaps even more important than knowing where you stand right now is tracking your net worth over time to see if you’re moving in the right direction.

Eventually, the goal is to grow your net worth to the point where you can live off the assets you’ve accumulated. When that happens, work is truly optional, and you’re completely financially independent.

There are three ways to grow your net worth:

Saving

In the early stages of your career, saving will drive most of your net worth growth. In order to translate your income into wealth, you need to save money so you can build assets. Your net worth isn’t determined by how much you make but by how much you keep.

Make a plan to save a portion of your income (15% to 20% is ideal). It’s the most important thing you can do to start growing your net worth. If every dollar of your paycheck is going toward living expenses, you’re not making any progress.

Your net worth won’t increase until you start setting aside money for yourself.

Debt Reduction

Debt can be a powerful tool that can aid you in buying assets that you wouldn’t have been able to afford through saving alone. Taking out debt may initially decrease your net worth, but it can provide you with an opportunity to grow that otherwise wouldn’t have been available.

Reducing debt directly increases your net worth. For those who are uncomfortable with debt, you can make extra payments to get rid of it as soon as possible. Or you can stick to your original payoff schedule and use your excess cash in other areas. You’d be surprised at how much progress you make by just making minimum payments on your loans. Every time you make a monthly debt payment, you’re growing your net worth.

Asset Growth

While saving and reducing debt will be the primary driver of net worth when you’re starting out, asset growth will do the majority of the heavy lifting later in your career.

As you buy assets, whether that’s a business, real estate, or stocks, the hope is that they’ll increase in value. Although you don’t really have control over how much your assets will grow, you can pick smart investments and stay the course. It’s impossible to predict how the real estate market or the stock market will perform from year to year, but over time, these markets have shown to be reliable. Keep buying and playing the long game.

Sketch by Carl Richards from The Behavior Gap

Even though growing your net worth is as simple as adding assets and reducing liabilities, it’s not easy to do. It takes time, discipline, and intentionality. Your progress may not always feel exciting, but remember that building wealth is a lifelong pursuit.

Save consistently. Manage debt wisely. Invest for the long term. And track your progress.

Thanks for reading!

Jake Elm, CFP® is a financial advisor at Dentist Advisors. Jake a graduate of Utah Valley University’s nationally ranked Personal Financial Planning program. As a financial advisor at Dentist Advisors, he provides dentists with fiduciary guidance related to investments, debt, savings, taxes, and insurance. Learn more about Jake.