At the beginning of April, I wrote about how the stock market had taken a tumble largely due to the consequences of the war with Iran. The S&P 500 dropped nearly 9% during the month of March, leading to a total decline of 7% for the year.

I also wrote that if you can understand that market dips are a normal part of investing, you can then try to shift your mindset to view those dips as opportunities.

Over the past 75 years, each time the stock market drops by 10%, the average one-year forward return has been 15%.

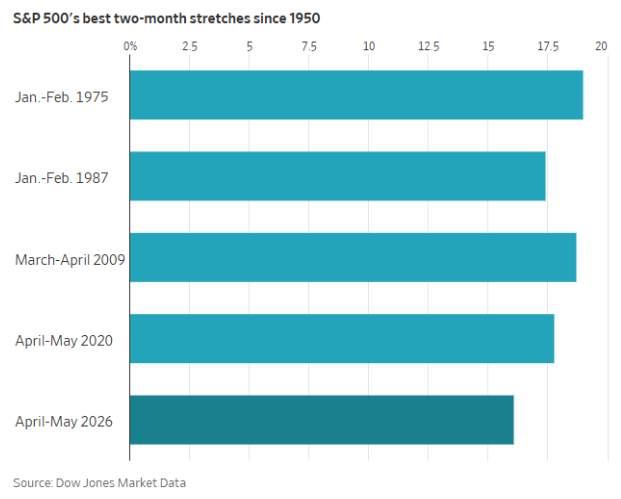

Well, this time it didn’t take a full year to reach that return mark. It only took two months.

From April 1st to May 29th, the S&P 500 grew by over 15%. As a matter of fact, it’s the 5th best two-month stretch since 1950:

Not a bad time to have your money invested.

Ironically, alongside this market boom over the past few years, the national average savings rate has been on a steady decline:

Since last April, the S&P 500 is up 49% since last April. Meanwhile, the average savings rate has declined from 5.5% to 2.6%.

One way of interpreting this falling savings rate is that the crunch of inflation is finally catching up with people. Americans are saving less because of higher prices and incomes not keeping pace.

I think that’s a valid take. There’s likely some of that happening here.

However, a different, maybe counterintuitive reading would be that because of the stock market boom, people don’t think they need to save as much.

A graph from Bank of America shows that personal savings rates tend to be negatively correlated with household wealth:

The more money people have, the less they feel like they need to save. The inverse is also true. When times are hard, people will spend less and save more. Just look at the crazy spike in savings during COVID. This has been a consistent trend over the past 35 years.

So a plunging savings rate can be a positive economic indicator. More often than not, it signals personal household wealth is growing.

Now, on an individual level, I wouldn’t necessarily recommend lowering your savings rate simply because your investment portfolio has had some nice gains recently.

If you’re still working toward financial independence or other financial goals, the combination of awesome stock market returns and a high savings rate can be a potent wealth-building formula.

Thanks for reading!

Jake Elm, CFP® is a financial advisor at Dentist Advisors. Jake a graduate of Utah Valley University’s nationally ranked Personal Financial Planning program. As a financial advisor at Dentist Advisors, he provides dentists with fiduciary guidance related to investments, debt, savings, taxes, and insurance. Learn more about Jake.