Compound interest gets talked about a lot in investing. And rightfully so. It’s what allows you to turn your modest, consistent investment contributions into large sums of wealth. Many people say the first time they saw a compound interest table or calculator it blew their mind and changed their outlook on investing.

The following tweet is an example of just how mind-boggling compound interest can be:

Investor A – saves $2K/year from age 26-65.

Investor B – saves $2K/year from age 19-26 and stops there.

Both achieve 10% annual return.

At age 65, who ends up with more money?

Investor A: $893,704 Investor B: $930,641

Another crazy compounding statistic is The Dow, an index that tracks 30 of the largest U.S. companies, has compounded at less than 0.03% a day since 1970 but is up more than 3,000% since then.

The magic of compound interest is such that Albert Einstein proclaimed:

“Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it.”

Yet, while compound interest is amazing, many fail to reap the rewards of it because of the time and patience it requires.

It requires time and patience because the majority of the gains from compounding come at the end. Building wealth through compound interest is the exact opposite of getting-rich-quick.

Here’s an example:

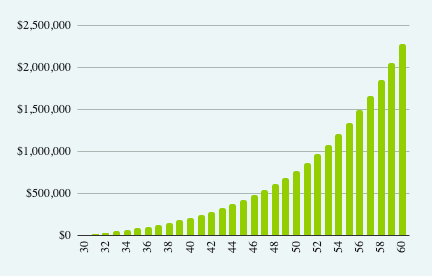

Let’s say you started investing $1,000 a month when you were 30. Given a 10% annual rate of return, at age 60 you’d have accumulated over $2.2 million. Pretty awesome.

Now, using those same numbers, let’s say you decided to stop investing at 50 instead of 60. After all, 20 long years of consistent investing feels like it should be sufficient. But that’s not the case. At age 50 you’d only have accumulated $766,000.

Here’s a graph of what the growth would look like:

You can see that the last 10 years are where all the magic happens.

Conversely, if you were to continue investing an additional ten years until age 70, you’d have increased your balance to a whopping $6.4 million.

“Understanding both the power of compound interest and the difficulty of getting it is the heart and soul of understanding a lot of things.” — Charlie Munger

Warren Buffett is widely considered the greatest investor of all time and currently has a net worth of $100 billion. The key to his success, and his secret, is that he began seriously investing when he was 10 years old. So he’s now been investing for three-quarters of a century.

As a thought experiment, let’s pretend he was a more normal person who spent his teens and 20s exploring the world and finding his passion and didn’t start investing until the age of 30. Let’s also say that he quit investing and retired when he was 60 to play golf and spend time with his grandkids.

What would his net worth be today? Not $100 billion, but somewhere around $11.9 million. That’s 99.9% less than his actual net worth today.

“My wealth has come from a combination of living in America, some lucky genes, and compound interest.” — Warren Buffett

The moral of the story is to start early and stop as late as possible.

I understand that patiently investing for a long time and letting compound interest work its magic is not the sexiest investment strategy. At least not at the beginning. For those just starting to save and invest, 30 years in the future might as well be never. It can be hard to get excited about projected wealth so far in the future.

However, I’m confident you won’t have a hard time being excited when you make it there. The best asset most investors have is time.

Thanks for reading!